- place of management;

- a branch;

- an office;

- a factory;

- a workshop, and

- a mine, an oil or gas well, a quarry or any other place of extraction of natural resources

- a building site or construction or installation project constitutes a permanent establishment only if it lasts more than twelve months

- the use of facilities solely for the purpose of storage, display or delivery of goodsor merchandise belonging to the enterprise;

- the maintenance of a stock of goods or merchandise belonging to the enterprisesolely for the purpose of storage, display or delivery;

- the maintenance of a stock of goods or merchandise belonging to the enterprisesolely for the purpose of processing by another enterprise;

- the maintenance of a fixed place of business solely for the purpose of purchasinggoods or merchandise or of collecting information, for the enterprise;

- the maintenance of a fixed place of business solely for the purpose of carryingon, for the enterprise, any other activity of a preparatory or auxiliary character;

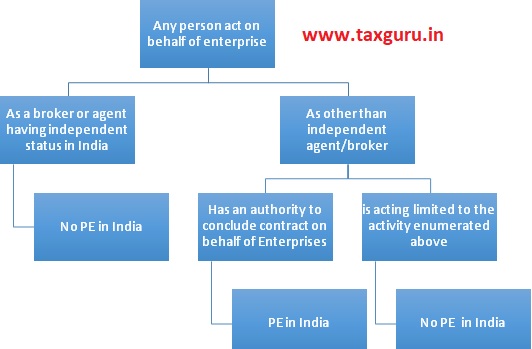

- One more point worth noting has been mentioned in Article 5 is, the fact that one enterprise resident of one country controls or is controlled by other enterprise in other country shall not itself constitute either company a ‘PE’ of the other. That means mere fact that a company is subsidiary or holding of other company does not make either company ‘PE’ of other. An enterprise has to undergo all the test as mentioned above to be held as PE.

- In the case of Adobe Systems Incorporated vs. Assistant Director of Income Tax (2016, Delhi HC), it was held that,

“A subsidiary company is an independent tax entity and is separately taxed for its income in the country of its domicile. In the present case, Adobe India is a separate assessee and is liable to pay tax on its income. The fact that a holding company in another contracting State exercises certain control and management over a subsidiary would not render the subsidiary as a PE of the holding company. This is expressly spelt out in paragraph 6 of article 5 of the Indo-US DTAA. [Para 28]”

“A subsidiary company is a separate tax entity does not mean that it could never constitute a PE of its holding company. In certain circumstances, where the specified parameters defining PE – in the present case article 5 of the Indo-US DTAA – are met, a subsidiary would constitute a PE of its holding company. However, in determining whether the requisite parameters are met, it is necessary to bear in mind that a subsidiary is a separate legal entity and its activities, the income from which are assessed in its hands at arm’s length pricing, cannot be the sole basis for the purposes of imputing the subsidiary to be a PE of its holding company.”

- To conclude, we can say that a foreign company, non-resident in India may be taxed in India if it is operating through a Permanent Establishment in India.

About the Author

Author is Amit Jindal, ACA working as Manager Taxation in Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India.